The Ultimate Guide To Moreira Team - 领英

Moreira Team Mortgage "/>Fastest What Is The Upfront Fee For Usda Loans

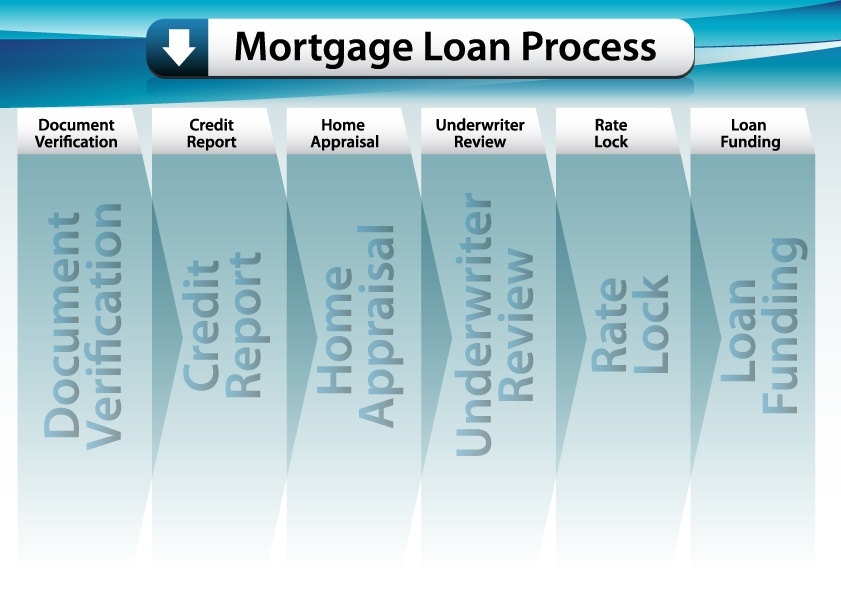

Little Known Facts About Moreira Team, MortgageRight Posts a 7-Step - Accesswire.

There are more residential or commercial property requirements with the direct loan than the guaranteed loan. For instance, the home must be 2,000 square feet or less and not have an in-ground swimming pool. Do I Receive a USDA Loan? To get a USDA loan, you have to meet certain requirements: Your earnings must be within 115% of the average household earnings limitations defined for your area (discover out if you're eligible here)You need to be a U.S.

Compared to conventional home loans, "the credit requirements are more versatile," states Cynthia Meyer, CFP, investor, and founder of fiduciary company, Real Life Preparation. Just how much money you have saved likewise matters, even if you qualify as low earnings. "If you can put 20% down, you typically won't have the ability to utilize this home loan choice," states D.

Alvaro Moreira (@moreira_team) - Twitter

What Are the Rates and Terms for a USDA Loan?Mortgage interest rates are low today across the market. Government-backed loans, such as USDA mortgages, are usually lower than conventional loans."Rates can be a half-point lower than an equivalent conventional home mortgage rate,"states Dan Green, founder and CEO of Homebuyer, a mortgage lending institution for novice house owners. When it comes to terms, USDA guaranteed loans are provided for just 30-year terms at fixed rates. Direct loans have repayment durations of as much as 33 years, with a 38 year-option available to low-income applicants who can't manage a 33-year term. Rates of interest for a direct loan are repaired and can be as low as 1 %when considering payment help. Because the majority of USDA customers have guaranteed loans, we'll offer instructions for that procedure here. If you have low earnings and are considering a loan straight through the USDA, we recommend examining your eligibility and contacting your regional USDA office, which will have an application available to you. 1. Identify your eligibility, Prior to you begin applying, determine if you satisfy the requirements for income, citizenship, financial obligation, and properties. If it's lower, check out ways of repairing your credit to increase your opportunities of getting a mortgage. 2. Find a USDA-approved lender, Next, you'll want to research study and evaluation terms offered from USDA-approved lenders. Numerous lenders use USDA loans, however they tend to be rare compared to the more popular FHA and VA loans. Additionally, you need to prepare to live in the house you purchase, because getaway